The financial services sector has become increasingly competitive in the last few decades as the popularity of big banks has waned and smaller boutique-style organizations have gained traction. Financial services like taking out a home loan, opening investment accounts, and refinancing are now offered by a wide variety of smaller financial institutions with easy-to-use technology, personalized customer service, and great rates.

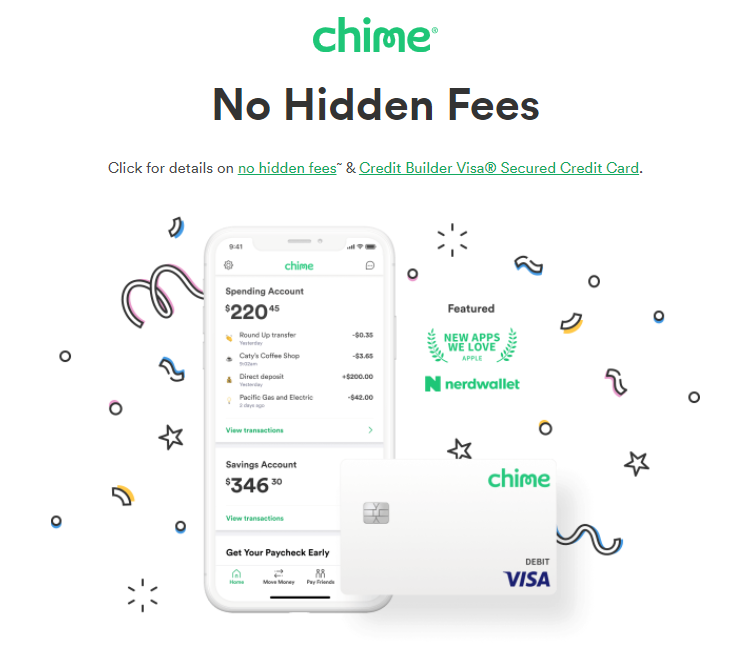

For example, Chime (see photo below) is a virtual bank that offers features that millennials crave like an intuitive mobile app, zero hidden fees, overdraft protection, high-yield savings, a credit-building credit card, and more. With all of these new financial service providers popping up every day, how can financial businesses stay ahead? With a focus on customer-centricity driven by virtual interviews, brands can discover what truly matters to their customers, boost loyalty, and stay ahead of the competition. Keep reading to find out when and how to conduct a customer interview for financial services.

When To Conduct Virtual Interviews

Customer interviews are a powerful tool that can help financial institutions get to the heart of their customers’ motivations, beliefs, and attitudes about banking. For instance, many aspects of banking are quite emotional such as a parent opening a child’s first bank account, purchasing a home, or buying a car. In these cases, it’s helpful to clarify what the customer expects, needs, and wants from your institution.

Customer Interview Project Outline: Home Loans

Objectives

Suppose a banking institution has noticed that their home loan applications have declined in recent months. They have been offering the same kinds of loan options for the last few years but feel now that it is time to re-evaluate their programs with the decline in applications. In this case, an in-depth customer interview would be helpful to determine what aspects of their home loans need improvement. This bank opts to interview current home loan customers about their experiences to see where they are falling short.

Questions

The bank’s objective is to uncover why they are experiencing a decline in home loan applications. Some examples of questions they may ask their current home loan customers about their experiences include:

- What made you decide to use our bank for your home loan?

For example, Our rates, technology, or customer-service ratings. - In what ways has your home loan met your expectations?

Maybe the payments are easy to make, statements are reliable, or customer service is easy to access - In what ways has your home loan not met your expectations?

Such as a confusing online portal, high loan rates, or inattentive customer service representatives. - What features would make you refinance with a different bank?

Potential responses may include lower rates, a better mobile application, or better customer service.

Conclusions

After completing customer interviews, the bank looks for commonalities and trends in the responses. They may notice, for example, that most current home loan customers are not satisfied with their mobile application and feel that other financial institutions offer more intuitive mobile platforms. In this case, the bank could use these findings to re-vamp their current application based on customer feedback.

To learn more about the financial services industry, check out our webinar, “Exploring the Drivers of Fragmented Loyalty in Financial Services.”